Profit from the secret signals in analyst research

Research analysts are regarded as some of the market’s best informed judges of shares. Employed by brokerages and advisory firms to study stocks, interpret news and dispense trading recommendations, they are a vital conduit of information between companies and investors.

A brief guide to consensus analyst forecast data

Analysts often slave away on long form research reports that are written solely for their high paying clients. What filters through to the rest of the market - and down to private investors that don’t have privileged access - are a few key metrics. The include:

Earnings estimate: what the predicted profit level will be for the next few years.

Recommendation: whether to buy, sell or hold the shares.

Every analyst who follows a company will issue these metrics to the market. At Stockopedia we publish the average or ‘consensus earnings estimate’ of all estimates in the market for a given company, and also the ‘consensus recommendation’.

Because analysts enjoy close access to company management teams, their opinions, recommendations and earnings forecasts are highly regarded. However, decades of work by academics has found that this advice isn’t always as reliable, accurate or valuable as you might expect. To get the most out of analyst research requires practising the art of reading between the lines.

Beware of Analyst Recommendations

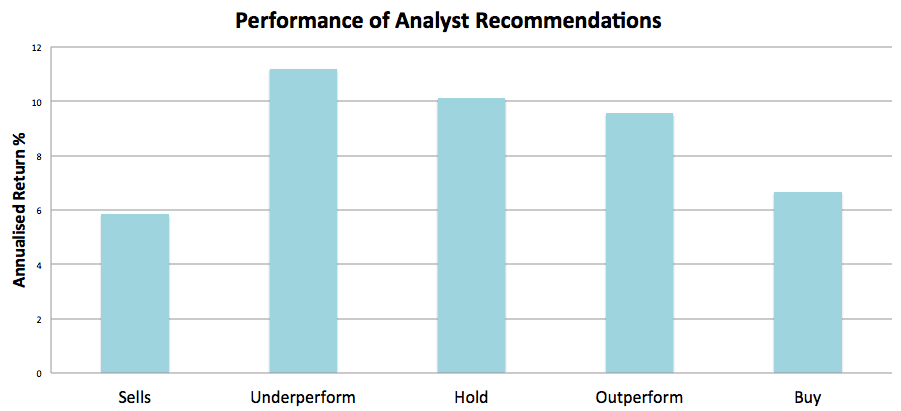

Scouring the market for companies rated ‘STRONG BUY’ among research analysts sounds like a smart investing strategy, but it isn’t. Of all the thousands of stock recommendations made each year, only around 10% ever advise selling a stock. This mighty imbalance indicates that analysts are hugely biased towards making positive recommendations about the companies they cover.

The truth is that analysts are often fundamentally conflicted. On the one hand they are required to produce objective research while on the other the companies they work for often need to keep up genial relationships with management. While ‘chinese walls’ are supposed to separate different parts of investment banks, analysts rarely seek to compromise the work of corporate finance departments who may aim to secure valuable investment banking work.

So while it may be exciting to see a ‘buy’ recommendation on a share of interest, the absolute level of these recommendations can often be meaningless. Indeed, tracking the performance of recommendations to ‘buy’ shows that they don’t outperform those to ‘hold’ and barely outperform those to ‘sell’. This is made incredibly clear in the chart below.

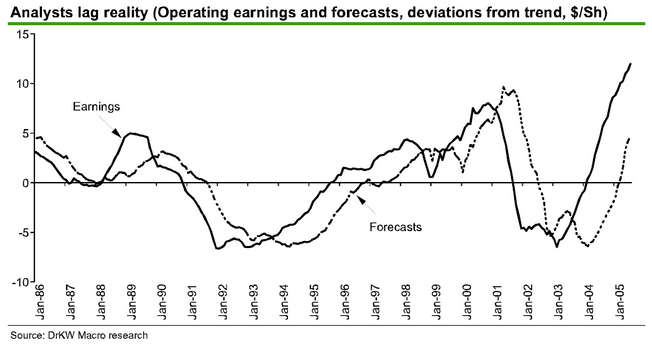

What’s more the predictions they do make tend to lag the market. Here’s a chart from highly regarded GMO fund manager James Montier and a quote that tells a very sad story!

”Analysts are terribly good at telling us what has just happened but of little use in telling us what is going to happen in the future.”

Academics have also found that analysts prefer recommending ‘glamour’ shares[1]. These are typically the ‘story’ stocks of the day that boast strong share prices, high growth and high share trading volumes. But these shares can become very expensive to buy. As well-drilled Stockopedia subscribers should know, buying overpriced shares can seriously damage potential future returns[2].

So if all this is true how on earth do you read between the lines?

Changes, Changes, Changes…

While analysts are often overly-optimistic, there are still reasons to take note of their opinions. This is because their research is a major contributor to one of the most powerful driving forces behind share prices - momentum.

Price momentum occurs when the market takes days, weeks or even months to properly price a stock to reflect its improved outlook. Traders and fund managers are often slow to react to new analyst coverage or simply can’t work out which analysts are best at spotting mispriced stocks. As a result the stock gradually drifts upwards in price, creating a buying opportunity for momentum investors.

This type of pricing inefficiency is most striking when analysts make or have to make changes. Changes to their recommendations, upgrades to their forecasts or are surprised by company performance.

For investors wanting to capitalise on the momentum effects driven by changing analyst sentiment, there are Three Key Rules to remember:

Rule 1. Wait for recommendation changes

While analyst buy recommendations barely outperform their sells but it would be a mistake to throw the baby out with the bathwater. When a respected analyst announces a big recommendation change it can create a big shift in the share price on the day of the announcement and often an ongoing share price drift[3].

When assessing changes of sentiment in analyst research, it’s important to distinguish between bold revisions and herding revisions. Bold revisions are made by analysts whose recommendation moves away from the consensus view of other analysts - signalling that they have new information. Herding revisions are those that merely move closer towards the consensus - signalling that they simply agree with other analysts. Analysts watch each other’s recommendations closely, seeking job safety by never straying too far from the herd. An analyst rarely puts their career on the line for a bold recommendation, so when they do it’s worth taking note.

Research shows that bold revisions can have a greater initial impact on prices, though the ongoing price drift is driven by the herding revisions. The most powerful boosts are seen in shares that are attracting the highest number of revised recommendations in recent weeks. These recommendation changes can be even more useful when combined with earnings estimate revisions.

Rule 2. Join the trend in earnings revisions

Nothing speaks more about the confidence of analysts than when they make upgrades to their earnings estimates for a stock. Changes to earnings estimates occur much more frequently than recommendation changes. With companies making regular trading announcements to the market, forecasts can be revised on a quarterly or even monthly basis.

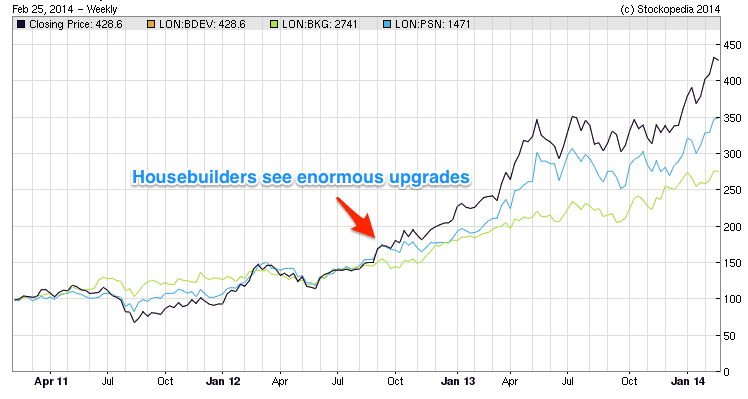

Case Study: Housebuilders see enormous Earnings Revisions

In late 2011 the UK housebuilding sector was flagged as hugely undervalued according to traditional valuation ratios. Most investors believed that the sector was in a secular bear phase as deleveraging continued. But as the economy started recovering, analysts in unison increased their earnings forecasts for the housebuilding sector faster than any other. This led to rapid revaluation of all housebuilders, with plenty of time for nimble private investors to gain.

A pan-European study into the impact of ‘Earnings Revisions’ found that stocks with the greatest number of upward revisions, net of downward revisions, achieved much higher returns than otherwise similar stocks[4]. A portfolio of shares in the highest 20% of net upward revisions outperformed the bottom 20% of upward revisions by more than 16% annually.

Importantly, this work confirmed that positive price momentum can be caused by analyst research. While earnings downgrades were very quickly priced-in by the market, investors were more cautious about upward revisions, knowing that analysts can be biased and over-optimistic. Because earnings revisions can take several months to be fully acknowledged by the market, investors have ample time to take advantage of them.

Rule 3. Act quickly on Earnings Surprises

Expectations of a stock’s financial performance are judged against the earnings per share (EPS) forecasts set by the consensus of analysts. Beating these expectations on results day is a sure fire way for companies to get a warm reception from shareholders. During results season it’s no surprise to see shares jumping 10% or more on the announcement of an ‘earnings surprise’.

Stocks that pull off surprises regularly see their prices drift higher for up to three months after reporting their results. This ‘post earnings announcement drift’ in share prices has been a startling discovery to academics. The publication of reams of research papers has led to many hedge funds basing their entire trading strategies on the anomaly.

In one study, the top 20% of shares in terms of upside earnings surprises outperformed the broader market by 3% over six months and the top 20% in terms of sales surprises outperformed by 2.6%. But a cross sample of the two together managed to outperform the market by an even more impressive 5.3%.

Why do shares continue to drift after earnings surprises?

An immediate jump in the price of a share following an earnings surprise can temporarily deter new investors from buying it. Both private investors and institutions can be very slow to react to new information as they come to terms with the idea of buying the share at a new high price. Meanwhile analysts often take as long as six months to incorporate earnings and revenue surprises into their models, leading to delays in new capital allocation.

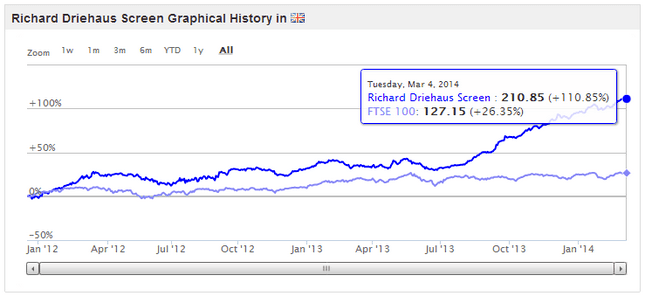

For those in the know, the tardy response of institutional investors to earnings surprises provides a highly effective trading opportunity for individual investors who understand the power of the ‘earnings surprise’. For instance, Richard Driehaus, one of the world’s most respected momentum investors, puts major emphasis on earnings growth and specifically looks for surprises as a ‘buy’ signal in his strategy. A glance at the performance of a portfolio based on his approach, as tracked by Stockopedia, reveals how successful it can be.

Investors should also be aware of the potential for earnings surprises to become a regular habit for some companies. Those that positively surprise the market with better than expected earnings in the past are more likely to do so again in the future. Meanwhile, serial disappointers are more likely to keep missing expectations. This kind of regularity means that earnings surprises are a driver of both earnings momentum and price momentum, which together are one of the stock market’s most potent forces.

Summary - Analysing the analysts

Analysts are undoubtedly some of the smartest thinkers in the City, with the huge advantage of having close contact with company management. Even so, deficiencies in the way research is produced and questions about its objectivity mean that investors must use it with care.

Fortunately, decades of scrutiny have revealed precisely where analyst research is at its most powerful. Typically this is when analysts - either alone or together - revise their recommendations or forecasts or when a company surprises the market with financial results that beat expectations. Studies have shown that it’s in these situations that share prices respond most significantly.

It’s essential to recognise that the market can be surprisingly slow to digest the full meaning of revised expectations and changes of opinion. This uncertainty about how important an upgraded recommendation or forecast really is means it can take many months for share prices to incorporate the change in sentiment. This positive momentum - where stocks that have recently risen often continue to rise in price - is not only proven and predictable but is also one of the most powerful drivers of future share gains in the market.

Overall, the key takeaway from the research into the influence of analysts is that investors must read between the lines. Analysts are regularly poor at predicting price movements. To profit from their expertise it’s necessary to ignore most of their recommendations and focus on the trends in sentiment that can trigger long term price rises.

- Brad Barber, Reuven Lehavy, Maureen McNichols and Brett Trueman. Can Investors Profit from the Prophets? Security Analyst Recommendations and Stock Returns.

- Narasimhan Jegadeesh, Joonghyuk Kim, Susan D. Krische and Charles M. C. Lee. Analyzing the Analysts: When Do Recommendations Add Value?.

- Kent L. Womack. Do Brokerage Analysts' Recommendations Have Investment Value?.

- Steven K. Todd and Phillip J. McKnight. Analyst Forecasts and the Cross-Section of European Stock Returns.